The increased influence of NGDP…

Scott Sumner has been described by The Atlantic as “the blogger who saved the economy” due to the influence he had over the Fed’s late 2012 QE3 program. You can see a great overview of the rise of Sumner here:

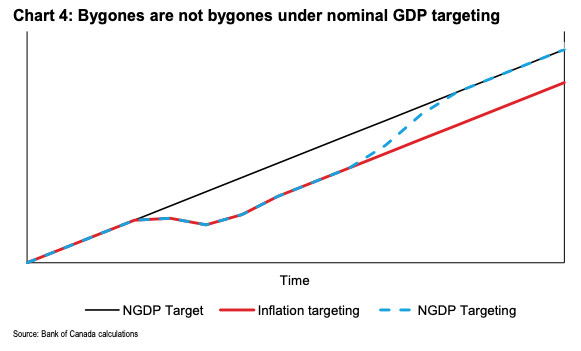

A key thing that he emphasises is that it’s not just the fact the nominal income is a more important variable for macro stability than price stability, but that the expected growth path of a variable is more important than a rate. In other words, if a central bank “misses” a 2% target the question is whether it tries to get back to 2% and consider that enough, or whether they try to get back to where things would have been had the 2% growth path continued. In technical terms NGDP advocates want a level target and, as Mark Carney’s chart below shows, to not let bygones be bygones.

(Astute readers will point out that you could have an inflation level target and achieve the same result, which is indeed the case. But for simplicity we compare the status quo inflation growth rate target and the potential NGDP level target).

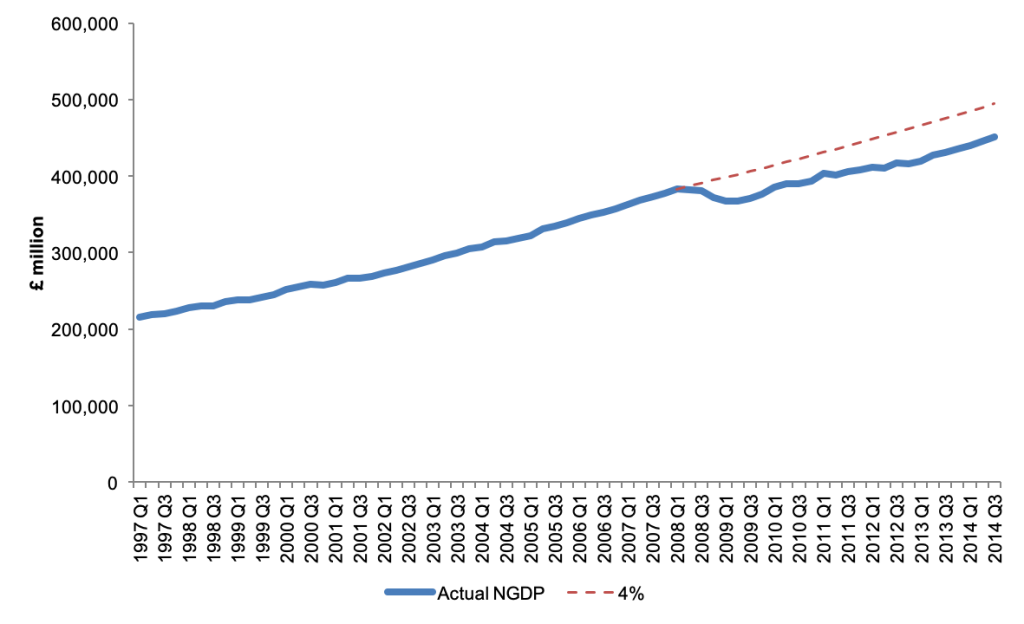

So even though thinking in growth rates is easier to communicate, the power of an NGDP level target is best shown when we look at absolute units. And as the chart below shows the UK deviated from a hypothetical 4% growth path and failed to catch back up again. That NGDP gap represents a permanent loss of economic activity relative to the public’s prior expectations, and forces an unnecessary and painful slowdown.

Source: ONS, own calculations