Working on NGDP targets

In May 2013 I organised a conference in Copenhagen, hosted by Danske Bank. It involved Lars Christensen as well as Sam Bowman and Ben Southwood from the Adam Smith Institute. Lars coined the term “Market Monetarism” and became known as an early and influential advocate via his famous blog, “The Market Monetarist“. Sam advocated an NGDP target in a letter published by the Financial Times in 2014. And here is a nice video of Ben Southwood explaining how a NGDP target would mean that central banks don’t have to try to work out which shocks to respond to and which to ignore:

Also around this time, in 2016, the ASI published my policy report, Sound Money, which contained an NGDP proposal for the UK.

Some of the key questions to address when considering an NGDP target are as follows:

- Should it be a growth rate target or a level target?

- Should it be set at a high rate (which gives monetary policy more room to manoeuvre, and requires less of an adjustment from nominal wages in a downturn) or a lower rate (which permits mild deflation when productivity is high, and has less distortions on non-indexed factors such as taxes on capital)?

- Should it focus on GDP or some other measure of economic activity such as transactions, or something like Average Weekly Earnings?

- Should it focus on GDP/T/AWE as whole or adjusted for population growth (i.e. on a per capita basis)?

Considering all of these factors, I advocated a 2% average growth in NGDP expectations over a 5 year rolling period. The mains reasons were:

- It retains the public’s understanding of real GDP and inflation in terms of growth rates, not levels

- 5 years is a long enough time period to be a de facto level target

- 5 years is a short enough period to fit into the political cycle (and therefore generate some short term accountability)

- A 2% rate hedges against central bank incompetence at the zero lower bound

- A 2% rate provides a small cushion against deflation (which rightly or wrongly is politically dangerous)

- A 2% rate is low enough to permits a mild deflation whenever productivity grows above 2%

- It avoids the need (for now) to set up complicated futures market

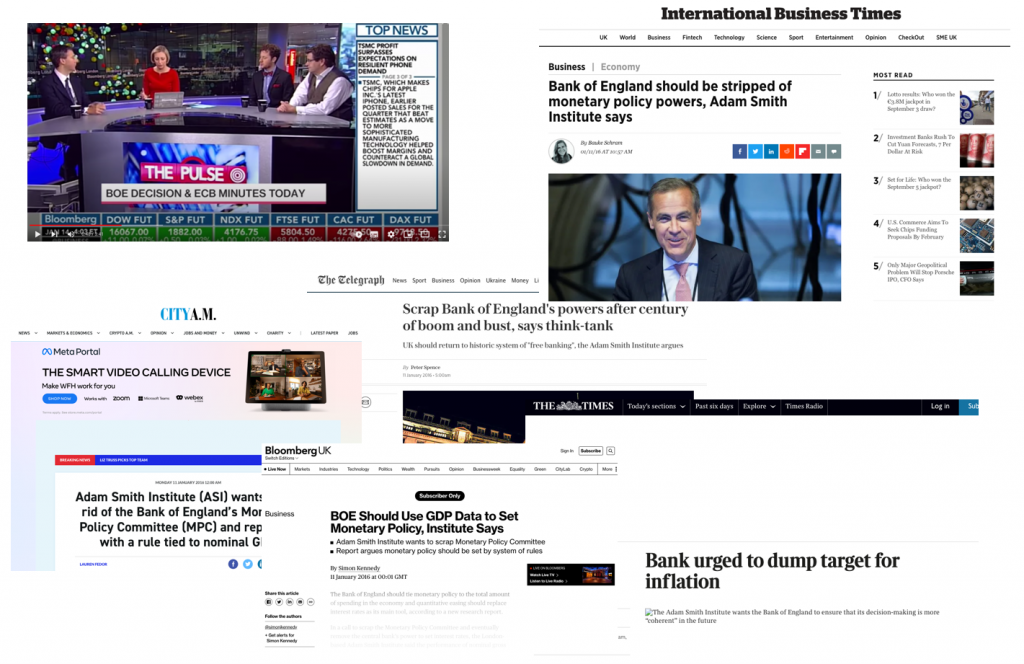

My proposal was trying to strike a balance between those who advocate that total spending is stable (i.e. a 0% growth target) and those who take the current inflation target (2%) and the typical long term real growth rate (~2%) to create a 4% NGDP target. But this idea didn’t catch on, and in hindsight it’s probably better to go for one or the other. Regardless, I was delighted to see that the proposals received extensive media coverage: